Introduction

Deciding whether to buy a home or continue renting is a major financial choice that can impact your future in significant ways. Many prospective buyers hesitate due to rising home prices and mortgage rates, but homeownership remains one of the most powerful wealth-building tools available. In fact, a report from Bank of America highlights that 70% of prospective buyers fear the long-term consequences of renting, including not building equity and dealing with rising rents.

If you’re on the fence, it’s important to understand why buying a home is still a smart investment in 2025. From financial security to long-term stability, owning a home offers numerous advantages that renting simply cannot match. In this comprehensive guide, we’ll break down the key benefits of homeownership and why now might be the best time to buy.

1. Building Wealth Through Home Equity

One of the greatest benefits of owning a home is the ability to build equity over time. When you rent, your monthly payments go directly to your landlord, with no long-term financial return. However, when you buy a home, your mortgage payments contribute to your ownership stake, increasing your net worth over time.

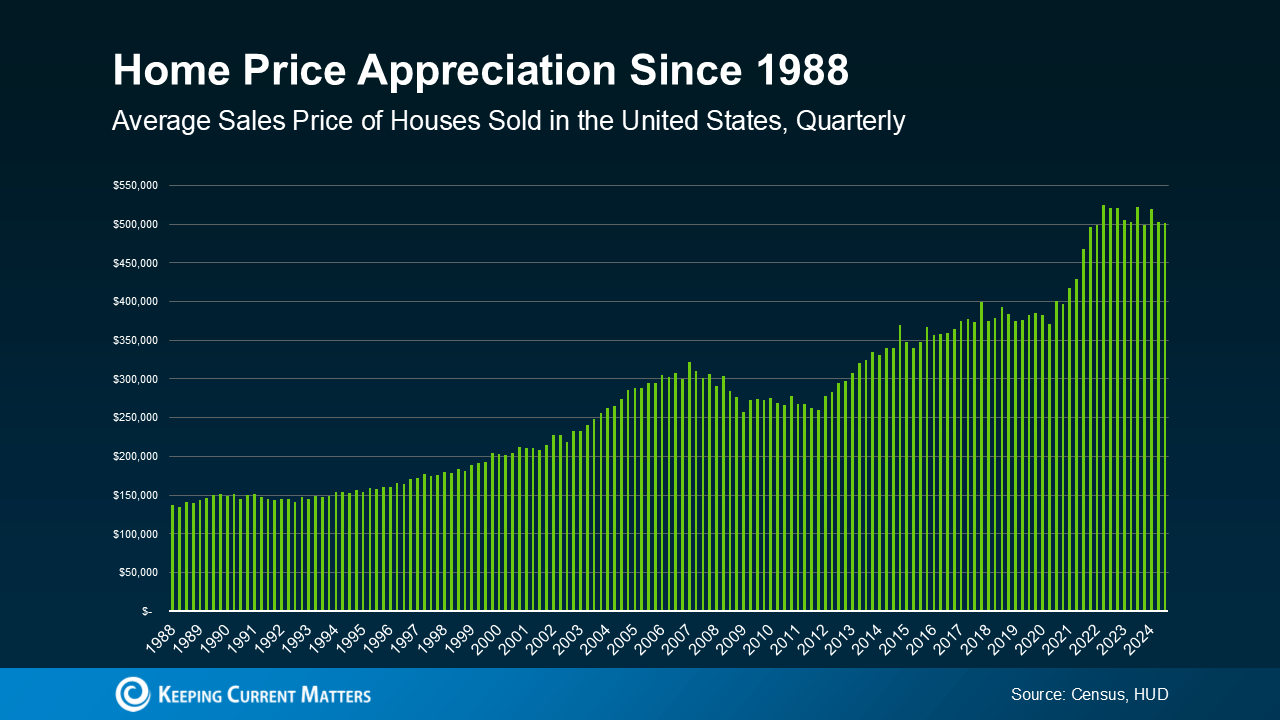

How Home Prices Have Grown Over Time

According to data from the Census and the Department of Housing and Urban Development (HUD), home prices have consistently appreciated over the decades:

This trend shows that homeownership not only provides a place to live but also serves as an appreciating asset that can increase in value, leading to significant financial gains in the long run.

2. Stability in Housing Costs Compared to Renting

Renting may feel like a more flexible option, but it comes with unpredictable costs. Rental prices have risen dramatically over the years, and tenants have little control over future increases. According to Census data, rents have consistently gone up decade after decade:

With a fixed-rate mortgage, homeownership offers stability. Your monthly mortgage payment remains predictable, protecting you from the uncertainty of rising rental costs. This stability is especially beneficial for families and individuals looking to establish long-term financial security.

3. Tax Benefits of Homeownership

Buying a home also comes with significant tax advantages that can help offset costs. Homeowners may be eligible for tax deductions on mortgage interest, property taxes, and even some home improvements.

Common Tax Deductions for Homeowners

-

Mortgage Interest Deduction: Homeowners can deduct interest paid on mortgage loans, reducing taxable income.

-

Property Tax Deduction: State and local property taxes can often be deducted, providing annual tax relief.

-

Capital Gains Exclusion: When selling a primary residence, homeowners can exclude up to $250,000 (or $500,000 for married couples) of capital gains from taxable income.

-

Home Office Deduction: If you work from home, you may be eligible for deductions on a portion of your mortgage and utility costs.

These financial incentives make homeownership even more attractive from a long-term financial perspective.

4. Generational Wealth and Financial Security

Homeownership has historically been a major driver of generational wealth. Owning property allows individuals to pass down assets to their children and grandchildren, creating long-term financial stability for future generations.

Homeownership vs. Renting for Wealth Accumulation

According to a report by the Federal Reserve, the median net worth of homeowners is nearly 40 times greater than that of renters. This significant wealth gap demonstrates how real estate can serve as a powerful financial tool for securing long-term prosperity.

If you’re thinking about your financial future and the legacy you want to leave, buying a home is a critical step toward financial independence.

The Long-Term Impact of Homeownership on Future Generations

One of the most powerful aspects of homeownership is that it provides financial security not just for the current owner but for their family as well. Unlike renting, where monthly payments contribute to a landlord’s wealth, owning a home ensures that wealth stays within the family. A paid-off home can serve as a financial safety net, providing future generations with an asset that can be sold, leveraged, or used to eliminate housing costs entirely.

As home values appreciate over time, the equity built in a property can be passed down, ensuring children and grandchildren have a solid financial foundation. Families who own homes are more likely to have access to financial resources for education, investments, and even starting businesses, further enhancing their financial security.

The Role of Real Estate in Closing the Wealth Gap

For many, real estate represents the most significant investment they will ever make. This investment has a compounding effect, allowing homeowners to increase their wealth while creating opportunities for their children. Studies have shown that children of homeowners are more likely to become homeowners themselves, continuing the cycle of financial stability.

Additionally, homeownership can play a crucial role in closing the wealth gap. Historically, families who have owned homes for multiple generations have been able to accumulate significantly more wealth than those who have rented long-term. By entering the housing market, first-time buyers create a pathway for future financial success, ensuring their families have access to valuable assets.

How to Leverage Homeownership for Generational Wealth

Building generational wealth through homeownership requires strategic planning. Homeowners can maximize their property’s financial benefits by:

-

Choosing High-Growth Markets: Purchasing a home in an area with strong appreciation rates increases the long-term value of the investment.

-

Maintaining the Property: Keeping a home in good condition ensures it retains value and remains a valuable asset for future generations.

-

Utilizing Home Equity: Homeowners can use equity for strategic investments, such as funding education or starting a business, further increasing financial opportunities for their families.

-

Creating Estate Plans: Proper estate planning ensures that property transfers smoothly to heirs, preventing legal complications and maximizing its financial benefits.

By understanding the long-term benefits of homeownership, individuals can make informed decisions that not only benefit themselves but also set up future generations for financial success.

5. Why 2025 Is a Smart Time to Buy

Beyond the general advantages of homeownership, 2025 presents unique opportunities for buyers who are ready to take the plunge.

1. More Inventory on the Market

Over the past few years, housing inventory has been tight, leading to bidding wars and soaring prices. However, experts predict that 2025 will see an increase in available homes, giving buyers more options and negotiating power.

2. Mortgage Rates Expected to Stabilize

After experiencing significant fluctuations in mortgage rates in 2022 and 2023, many industry experts anticipate a period of stability or slight declines in interest rates, making homeownership more accessible for buyers.

3. More Favorable Market Conditions

The market is expected to shift slightly in favor of buyers, providing opportunities to negotiate better deals, request seller concessions, and secure more favorable terms on home purchases.

6. Overcoming Common Fears About Buying a Home

If you’re still hesitant, it’s important to address some of the most common concerns about homeownership.

Concern #1: Affordability

Many buyers worry about affordability, especially with high home prices. However, there are several programs available to assist first-time homebuyers, including:

-

FHA loans (requiring as little as 3.5% down)

-

VA loans (offering zero-down options for eligible veterans)

-

State and local down payment assistance programs

Concern #2: Market Fluctuations

While the housing market has its ups and downs, real estate historically appreciates over time. Long-term ownership mitigates the impact of short-term market fluctuations.

Concern #3: Maintenance Costs

Owning a home does come with maintenance responsibilities, but setting aside an emergency fund and budgeting for repairs can help manage unexpected expenses.

7. Steps to Take Before Buying a Home

If you’re considering homeownership, here are some key steps to take before making the leap:

Step 1: Assess Your Finances

-

Check your credit score and work on improving it if necessary.

-

Determine how much you can afford based on your income and expenses.

-

Save for a down payment and closing costs.

Step 2: Research the Market

-

Look at homes in your desired area to understand pricing trends.

-

Consider different neighborhoods and their long-term investment potential.

Step 3: Get Pre-Approved for a Mortgage

-

Speak with a lender to determine your loan eligibility.

-

Understand different mortgage options and interest rates.

Step 4: Work with a Real Estate Agent

-

A knowledgeable agent can help you navigate the homebuying process, negotiate deals, and find the best property for your needs.

Conclusion

Buying a home is one of the most significant financial decisions you’ll ever make. While renting offers short-term convenience, homeownership provides long-term financial stability, equity building, and wealth accumulation. With 2025 presenting unique opportunities for buyers, now may be the perfect time to explore homeownership.

If you’re ready to take the next step, visit my website Hello Scottsdale Arizona or contact me, Denise to discuss your options and find the right home for you.